Kristine Rutkowski, Plan Manager

The following information is intended to provide background information on the requirements for financial industry professionals regarding FATCA/CRS reporting requirements. This may assist you and your clients when investors have foreign tax reporting obligations.

Foreign tax reporting regulations:

The Foreign Account Tax Compliance Act (FATCA) is a U.S. legislation which requires non-U.S. financial institutions to provide the U.S. Internal Revenue Service (IRS) with information on certain U.S. persons who have invested in accounts outside of the U.S., and for certain non-U.S. entities to provide information on any U.S. owners. In Canada, reporting of U.S. tax persons is done through the Canada Revenue Agency (CRA).

The Common Reporting Standard (CRS) requires all Canadian financial institutions to provide the Canada Revenue Agency (CRA) with information on accounts held by non-residents of Canada (non-U.S.).

Applicable accounts:

Based on the FATCA and CRS Guidance documents, Mackenzie as a fund company is required to obtain FATCA and CRS information on Client Name non-registered accounts for the purposes of reporting it to CRA. Canadian registered plans are exempt from FATCA and CRS reporting.

Account Type |

Who is required to complete FATCA and CRS Information? |

Individual or joint account |

Individuals, all members of a joint relationship

|

Informal Trust (ITF) account |

Settlors, trustees, protectors, beneficiaries, and any other natural persons exercising ultimate effective control over the Informal Trust. |

Sole Proprietorships |

Single Owner of proprietorship |

Corporations, Partnerships, Estates, Formal Trusts and Associations. |

Natural persons who exercise direct or indirect control. (Please see RC519 Annex section for more detailed information.) |

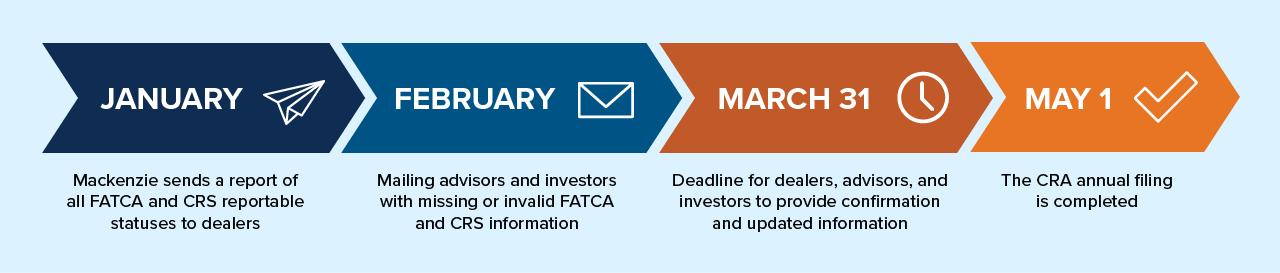

Annual review and filing:

On an annual basis, Mackenzie Investments completes annual reviews of all Client Name non-registered accounts with Dealers and Investors. This process ensures the information we have on file is correct prior to reporting information to the CRA.

Timeline

Self-certification (to obtain FATCA/CRS information)

Investors establishing new non-registered accounts are required to self-certify their tax status or tax residency (Canadian, non-resident; or U.S. tax person). Any client who is considered a U.S. citizen, U.S. resident, or resident of another jurisdiction for tax purposes is required to provide a Tax Information Number (TIN) of that jurisdiction.

Self -certification is required at time of account set up, and when a “change in circumstance” occurs.

Note: Change in circumstance includes a change or addition of information that affects the FATCA or CRS status of the investor. For example: A change in legal or mailing address.

Dealer Responsibilities:

The most recent CRA guidance advises that the dealers are responsible to obtain and maintain investor(s) self-certification information. Dealers are then required to pass the self-certification information for all Investors on to Financial Institutions. This is required for both 'reportable' and 'non-reportable' Investors. Previously, dealers were only responsible to provide information for Investors who were considered reportable under FATCA or CRS.

Information sharing methods:

- Mackenzie's Tax Residency Confirmation Form

- Electronically via Wire orders or Non-Financial Updates (NFU)

- CRA Tax Residency Confirmation form RC518 (Individual)/RC519(Entities)form

- A dealer's own Individual Self-Certification or application

For more information on FATCA and CRS, please visit the following pages on the CRA website: