Near the end of every year, it can be a good idea to examine your portfolio and see what has worked and what hasn’t. If one of the ETFs in your taxable account has experienced a decline, you might want to consider a tax-loss harvesting strategy.

If you’re smart about tax-loss harvesting, you could keep your investments on track and reduce your taxes as well.

What is tax-loss harvesting?

Firstly, tax-loss harvesting is only relevant for investors who hold assets in non-registered accounts. If all your investments are in government-registered accounts such as an RRSP, RESP or TFSA, tax-loss harvesting doesn’t apply, as these assets are already growing tax-free, or tax-deferred. However, it is wise to reassess assets that are underperforming, so you may want to read on.

At some point, for non-registered accounts, you will want to sell investments that have made gains, and there will be tax implications. Typically, you can expect to pay tax on 50% of the gain, payable at your marginal tax rate,1 (which depends on your income and home province).

This is a considerable saving, leaving you with more money to stay invested.

The superficial loss rule and how to stay onside

Selling a loss-making asset to save money on tax can potentially upset the balance of your portfolio, so you may want to consider reinvesting the money in a similar asset to maintain your asset allocation. However, the CRA’s superficial loss rule2 states that you cannot buy the same or identical asset within 30 calendar days after the sale. If you ignore the rule, you won’t be able to offset the loss against your gains.

This could mean that you miss out on any potential gains that the sold asset might make over the next 30-day period.

There is a solution: you can remain invested by buying an asset that covers the same asset class, so long as it is composed differently. You could then sell it after 30 days and reinvest in your old asset, or you could simply hold on to the new asset.

One simple way to reinvest in a sector that you have sold for tax-loss harvesting purposes is to invest in a different index.

For example, let’s say you once invested $20,000 in a fund that tracks the FTSE China 50 Index (for example, the iShares China Index ETF) and it has taken a $5,000 loss since the initial purchase. You may want to sell it to capture that loss for tax purposes, but you think that Chinese equities may be on the verge of recovery.

You could invest in an ETF that tracks a different Chinese equities index, such as the CSI 300 Index (for example, the Mackenzie China A-Shares CSI 300 Index ETF).

The replacement ETF provides exposure to China’s equity markets, so it may capture similar performance to the original fund if the Chinese equity market recovers. Because the CSI 300 follows different rules and includes an expanded opportunity set, you could potentially invest in it without breaking the superficial loss rule.

Why tax-loss harvesting is different this year

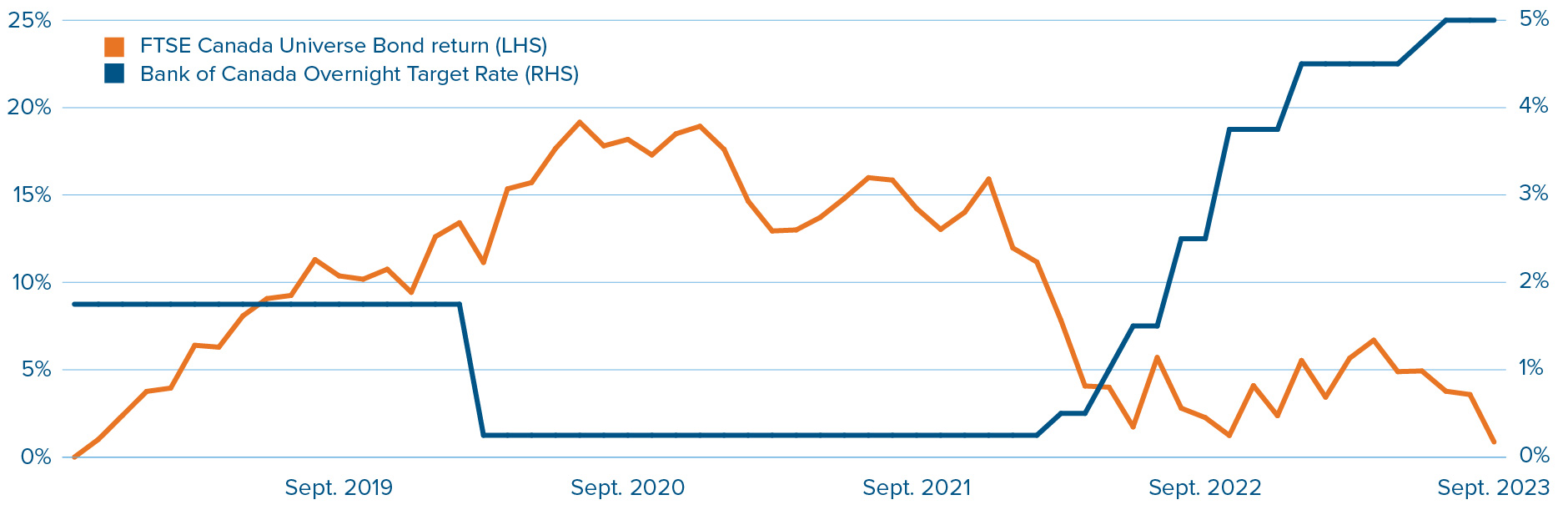

This year, we continued to see central banks increasing interest rates in order to curb inflation, which has also continued to negatively impact core fixed income returns. Bonds have an inverse relationship with interest rates—as interest rates go up, then bond prices go down, and vice versa.

Relationship between bond returns and interest rate movements

Source: Bloomberg as of September 30, 2023.

One of the main takeaways from the chart above is that, if you were to buy a Canadian core fixed income ETF anytime within the last five years, and are still holding, you are most likely looking at a loss.

You could take this opportunity to capture the loss within your fixed income portfolio to generate a tax benefit. Let’s say that two years ago, you invested $10,000 in an ETF that tracks the FTSE Canada Universe Bond Index, as your core bond holding. You may have accrued a loss of 17.12%3. Selling this holding would result in a loss of $1,712 — with the 50% inclusion rate, that’s a loss of $856 that could offset a future capital gain. Assuming the highest combined marginal tax rate of 53.53% (in Ontario), that results in an estimated tax saving of $458.22.

You would also receive $8,288 (minus any commissions) from the sale of the ETF, which you could immediately reinvest into a different core bond holding, like Mackenzie Canadian Aggregate Bond Index ETF (QBB). You would not run afoul of the superficial loss rule, because QBB tracks the Solactive Canadian Float Adjusted Universe Bond Index, which employs a different methodology to provide exposure to the Canadian bond universe.

You can also use this opportunity to reorient your fixed income allocation to better align for future market conditions. For example, if you believe interest rates will eventually fall, having a higher duration fixed income solution might offer more upside potential (i.e., the higher duration, the more sensitive to changes in interest rates).

Getting started with tax-loss harvesting

You have until two trading days before the end of the year to sell assets to qualify for tax-loss harvesting, however, it is recommended that investors do this quarterly. Harvesting losses as they occur may help to offset your eventual gains. Plus, losses can be carried over indefinitely, so they can offset future gains as well.

You should always talk to your accountant/tax professional and your financial advisor before deciding on the right tax-loss harvesting strategy for your unique situation.

Financial advisors can also contact their Mackenzie sales team, or login to our Continuing Education Centre, for accredited content on helping their clients harvest their tax losses more effectively.

Source:

1. Mackenzie Investments, as of January 2023.

2. Government of Canada, as of January 2023.

3. iShares Core Canadian Universe Bond Index ETF (XBB) based on 2-year price return from Bloomberg, as of September 28, 2023.

Commissions, management fees, brokerage fees and expenses all may be associated with Exchange Traded Funds. Please read the prospectus before investing. Exchange Traded Funds are not guaranteed, their values change frequently and past performance may not be repeated.

The content of this article (including facts, views, opinions, recommendations, descriptions of or references to, products or securities) is not to be used or construed as investment advice, as an offer to sell or the solicitation of an offer to buy, or an endorsement, recommendation or sponsorship of any entity or security cited. Although we endeavour to ensure its accuracy and completeness, we assume no responsibility for any reliance upon it.

This should not be construed to be legal or tax advice, as each client’s situation is different. Please consult your own legal and tax advisor. This article may contain forward-looking information which reflect our or third-party current expectations or forecasts of future events. Forward-looking information is inherently subject to, among other things, risks, uncertainties and assumptions that could cause actual results to differ materially from those expressed herein. These risks, uncertainties and assumptions include, without limitation, general economic, political and market factors, interest and foreign exchange rates, the volatility of equity and capital markets, business competition, technological change, changes in government regulations, changes in tax laws, unexpected judicial or regulatory proceedings and catastrophic events. Please consider these and other factors carefully and not place undue reliance on forward-looking information. The forward-looking information contained herein is current only as of October 13, 2023. There should be no expectation that such information will in all circumstances be updated, supplemented or revised whether as a result of new information, changing circumstances, future events or otherwise.

The Mackenzie ETFs are not sponsored, promoted, sold or supported in any other manner by Solactive nor does Solactive offer any express or implicit guarantee or assurance either with regard to the results of using the Indices, trade marks and/or the price of an Index at any time or in any other respect. The Solactive Indices are calculated and published by Solactive. Solactive uses its best efforts to ensure that the Indices are calculated correctly. Irrespective of its obligations towards the Mackenzie ETFs, Solactive has no obligation to point out errors in the Indices to third parties including but not limited to investors and/or financial intermediaries of the Mackenzie ETFs. Neither publication of the Solactive Indices by Solactive nor the licensing of the Indices or related trade mark(s) for the purpose of use in connection with the Mackenzie ETFs constitutes a recommendation by Solactive to invest capital in said Mackenzie ETFs nor does it in any way represent an assurance or opinion of Solactive with regard to any investment in these Mackenzie ETFs.

All rights in the CSI 300 Index ("Index") vest in China Securities Index Company ("CSI"). "CSI 300®" is a trade mark of CSI. CSI does not make any warranties, express or implied, regarding the accuracy or completeness of any data related to the Index. CSI is not liable to any person for any error of the Index (whether due to negligence or otherwise), nor shall it be under any obligation to advise any person of any error therein. The Fund based on the Index is in no way sponsored, endorsed, sold or promoted by CSI and CSI shall not have any liability with respect thereto.