Written by the Mackenzie Fixed Income Team

Key Highlights

- The Bank of Canada is likely to adopt an accommodative policy stance, with a potential rate cut in December influenced by sluggish economy and weaker currency.

- The second Trump administration's policies and new tariffs could impact Fed rate decisions, with potential challenges for emerging market fixed income due to higher Fed rates and a stronger USD.

- Favorable outlook for Brazil government bonds on valuations and currency intervention and New Zealand sovereign bonds due to expected aggressive rate cuts. Exposure to South Africa government bonds has been a key contributor.

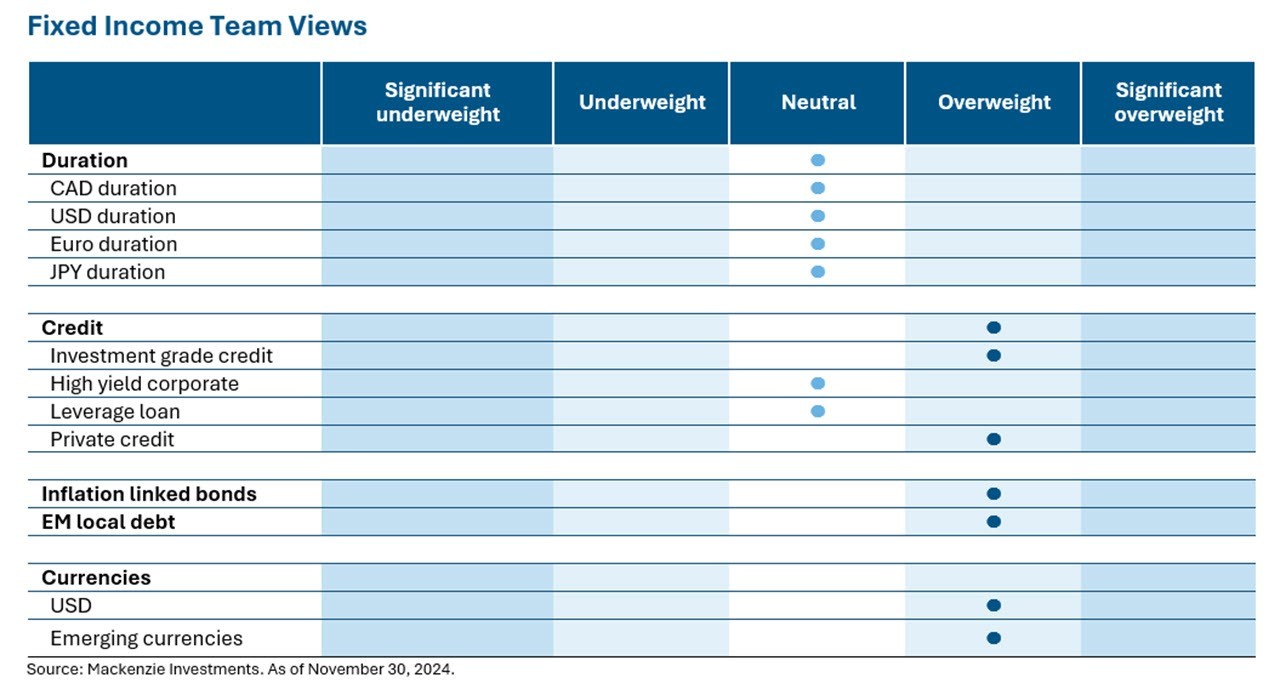

- Prefer high-grade Canadian corporate bonds at the short end of the yield curve. The team remains cautious on long-duration bonds, expecting yields to rise long term due to an improved US economic outlook.

Duration and Curve Positioning

Canada’s underlying economy remains quite weak buoyed exclusively by government deficits to keep things afloat. Despite the impact of stimulus, the economy remains meaningfully below potential and strengthens the BoC’s argument to reach a neutral or accommodative policy stance as fast as possible. Sluggish Canadian GDP data has led to coin toss between 25 and 50 bps of December rate cut. However, the weakening domestic currency with USDCAD breaking the 1.40 mark makes it harder to significantly diverge against the Fed. Lower rates are still needed, it is just a question of the pace at which those rate cuts are delivered. We expect high volume of news from the second Trump administration hence understanding the signal versus noise in economic data will be crucial for making informed policy decisions. The next Fed rate cut could happen in December, but the Fed is considering the potential inflationary impact of new tariffs and tax cuts under Trump administration, which could influence their decision to pause or skip rate cuts in early 2025. We expect 2025 to likely be challenging for EM fixed income led by tariffs, higher Fed rates and stronger USD. We favour our exposure to Brazil government bonds given the valuation and expectation of currency intervention by the central bank. We favour our sovereign global exposure to New Zealand as it seeks to revive its economy with a dovish monetary policy. The Reserve Bank of New Zealand has now lowered rates by 125 bps in little more than three months, making it one of the most aggressive among its western peers with expectation of faster and deeper rate cuts in 2025.

Central Bank Watch

US Fed (Fed)

As widely expected, the Fed cut rates by 25 bps in its November meeting, setting the target rate to 4.50%-4.75%. The cut came as Fed is now increasingly confident of inflationary trajectory less so about the labor market. With continued US economic exceptionalism and resilient earnings market participants seem to have scaled back expectations for future rate cuts. During the month, headline inflation for Oct at 2.6%, and Fed’s preferred measure - Core PCE at 2.8%, stayed stubborn and higher than the Fed target, backing a cautious approach. Incoming Trump administration policies including tax cuts and tariffs is likely to keep the yields elevated and the curve to be steeper on prospects of higher longer term inflation. The US 10-year treasury yield is now higher by ~60 bps from its September lows.

Bank of Canada (BoC)

Canadian bond yields declined led by weaker economic data. During the month the BoC’s preferred measure, headline inflation printed at 2.0%, within the target range of 1%-3%. The unemployment rate continued to remain elevated at 6.5%, supporting the case for continued rate cuts by BoC. This may potentially lead to a wider divergence with our US neighbours. Which further accentuates the risk of a weaker looney amid proposed tariff threats from the recently elected US President. These proposed tariffs could have significant economic impacts on Canada, potentially increasing costs for Canadian exporters and consumers.

European Central Bank (ECB)

Unemployment in the eurozone remains at historic lows, which is likely to influence the ECB's cautious approach to reducing interest rates. In October, the unemployment rate in Eurozone was 6.3%, marking the third consecutive month of record low unemployment. The ECB has started to lower interest rates and is expected to continue doing so at its upcoming policy meeting. The extent of the rate cut is still undecided, but persistently low unemployment supports the case for a 25bps cut in its upcoming December meeting. Markets in the US and Europe - from yields to exchange rates - have diverged since Trump's election win. Traders are weighing prospects of a stronger US growth and a hawkish Fed against a softer policy outlook from ECB.

Bank of Japan (BoJ)

Japan government bond yields rose as inflation was held above the central bank’s target. Consumer prices rose 2.3% in October driven partly by expensive imports, food prices and consumption even as electricity and gas prices was lower. The 2-year yield reached its highest level since 2008, while the 10-year yield increased to 1.075% following BoJ Governor Ueda's comments, hinting at a potential rate hike soon. Market now indicates a 60% likelihood of a rate hike in December, with the probability climbing to nearly 90% by January. We anticipate that the expected narrowing of the interest rate gap between the US and Japan, and consequently the yield differentials, will reduce the appeal of the carry trade. Strategy where investors borrow in Japan to invest in higher-yielding markets, may become less attractive.

Emerging Markets (EM)

Brazil bond yields rose near the end of the month as the Lula administration’s underwhelming commitment to fiscal spending cuts led to a significant deterioration in market sentiment. Since the government announced a spending package, Brazil local currency has sold off by 4.7% and market pricing of the terminal rate has risen more than 60 bps. Currency weakness has caused a significant jump in inflation expectations, especially against a backdrop of overheated domestic demand. South African bond market outperformed its EM peers and have remained broadly constructive on since the government formation. Although ZAR has lost some ground since Trump’s victory, we expect SA central bank to ease monetary policy in lieu of lower inflation.

Credit Market Performance

Investment Grade Credit (IG)

With the favorable backdrop for risk assets in November, CA IG bonds outperformed US IG with returns of 1.67% and +1.20% respectively. While the tighter spreads have led to expensive valuations it has propelled demand for certain idiosyncratic credits and high-beta sectors. We prefer to be invested in high-grade (low beta) corporate bonds at the short end of the Canadian curve. Continued rate cuts are the base case for Canada, and we see further potential for significant price appreciation of these securities.

High Yield Bonds (HY)

In November, the US HY index achieved a gain of +1.20%, with CCC-rated bonds (+1.78%) outperforming Single B-rated (+1.16%) and BB-rated bonds (+1.09%). During the period, US HY bond yields and spreads decreased by 16 bps and 14 bps, respectively, reaching 7.38% and 298 bps. Notably, HY bond spreads dipped below 300 basis points for the first time since July 2007, driven by diminishing growth concerns, a generally positive earnings season, and increased macroeconomic clarity following the US election results.

Leveraged Loans (LL)

The US LL gained +0.83% in November driven coupon clipping (+0.69%) and small price appreciation. November’s higher market value gains mitigated a decline in interest return following the 75 bps rate cuts. By the end of November, the three-month term Sofr had declined to roughly 4.5% from just under 5% in the first half of September and from 5.4% a year ago. The market returns were fueled by exceptionally strong demand from both CLOs and retail funds. Retail investors pumped nearly $5 billion into the loan asset class — the highest level since the Fed rate hikes began in 2022. A record number of $191B CLOs were priced year to date.

Bond Stories

High Yield Bond – Coinbase

Coinbase is a leading provider of end-to-end financial infrastructure and technology for cryptocurrencies and is best known for its centralized exchange platform, which is the largest in the U.S. in terms of volume. The 2031 bonds have been very volatile over the years, trading as low as 50 cents on the dollar when cryptocurrencies crashed in 2022. Despite the volatility, we maintained high conviction that the business would recover, driven by new revenue streams from its own Layer 2 blockchain on Ethereum and as a custodian for Bitcoin (and later Ethereum) ETFs launched in the US, with further support from a broader recovery in the cryptocurrency industry that would reignite volumes in dollar terms. Our conviction was tested when the company launched a tender in September 2023 to buy back these bonds at $67.5, but we rejected the deal to maintain exposure to the company’s recovery. This turned out to be a good decision as our recovery thesis played out over the following months. In November, cryptocurrency prices surged on the back of Donald Trump’s election, and the bonds gained another 2 points for the month. We are currently the third largest publicly reporting holder of the bonds with a $60mm position, and the November move made them a notable contributor for our funds.

Leveraged Loan – MoneyGram

MoneyGram International Inc. is a global leader in money transfer, operating in approximately 200 countries and territories with over 450,000 agent locations and digital services in more than 100 countries. The appointment of new CEO Anthony Soohoo brought a renewed focus on purpose, customers, and impact, with immediate efforts on optimizing strategies. Despite a cybersecurity incident in late September that temporarily disrupted operations, the company quickly restored normalcy and filed a cyber insurance claim to recoup losses. MoneyGram continued to innovate, launching the MoneyGram Wallet and expanding services in the US and Brazil, demonstrating a strong commitment to digital growth. Digital revenue remains a key driver, accounting for over 30% of total money transfer revenue and more than 50% of transactions. While high leverage and regulatory compliance challenges persist, the outlook remains stable, supported by MoneyGram's market position, adequate liquidity, and strategic focus on digital transformation.

ESG – Denali Term loan

Denali is a specialty waste management business that converts organic waste into agricultural and horticultural products such as compost and mulch. The company's term loan came under pressure during the first half of 2024 after it reported disappointing results in May 2024 in two of its operating segments. Despite the volatility, we continued to hold significant exposure to the name, given that 90% of the business provides recurring, non-discretionary services with high barriers to entry. Additionally, the company benefits from good ESG tailwinds and was trading at an attractive yield of 15.5%. Our thesis played out in November when management reported better than expected Q3 earnings, specifically noting improvements in one of the two operating segments. This resulted in the term loan increasing by 4 points in November.

We favor this company from an ESG perspective due to its impressive recycling efforts, converting 7 million tons of material in 2023 into animal feed, biofuel, mulch, and other industrial products. From a safety perspective, the company also reduced total recordable incidents by 50% from 2022. Finally, despite being privately owned, we appreciate the company's commitment to transparency through its annual sustainability report.

Commissions, trailing commissions, management fees, and expenses all may be associated with mutual fund investments. Please read the prospectus before investing. The indicated rates of return are the historical annual compounded total returns as of November 30, 2024, including changes in share value and reinvestment of all distributions and does not take into account sales, redemption, distribution, or optional charges or income taxes payable by any security holder that would have reduced returns. Mutual funds are not guaranteed, their values change frequently, and past performance may not be repeated. Index performance does not include the impact of fees, commissions, and expenses that would be payable by investors in the investment products that seek to track an index.

Index performance does not include the impact of fees, commissions, and expenses that would be payable by investors in investment products that seek to track an index.

This document may contain forward-looking information which reflect our or third party current expectations or forecasts of future events. Forward-looking information is inherently subject to, among other things, risks, uncertainties and assumptions that could cause actual results to differ materially from those expressed herein. These risks, uncertainties and assumptions include, without limitation, general economic, political and market factors, interest and foreign exchange rates, the volatility of equity and capital markets, business competition, technological change, changes in government regulations, changes in tax laws, unexpected judicial or regulatory proceedings and catastrophic events. Please consider these and other factors carefully and not place undue reliance on forward-looking information. The forward-looking information contained herein is current only as of November 30, 2024. There should be no expectation that such information will in all circumstances be updated, supplemented or revised whether as a result of new information, changing circumstances, future events or otherwise.

The content of this commentary (including facts, views, opinions, recommendations, descriptions of or references to, products or securities) is not to be used or construed as investment advice, as an offer to sell or the solicitation of an offer to buy, or an endorsement, recommendation or sponsorship of any entity or security cited. Although we endeavour to ensure its accuracy and completeness, we assume no responsibility for any reliance upon it.

All information is historical and not indicative of future results. Current performance may be lower or higher than the quoted past performance, which cannot guarantee results. Share price, principal value, and return will vary, and you may have a gain or a loss when you sell your shares. Performance assumes reinvestment of distributions and does not account for taxes. Performance may not reflect any expense limitation or subsidies currently in effect. Short-term trading fees may apply.

This material is for informational and educational purposes only. It is not a recommendation of any specific investment product, strategy, or decision, and is not intended to suggest taking or refraining from any course of action. It is not intended to address the needs, circumstances, and objectives of any specific investor. Mackenzie Investments, which earns fees when clients select its products and services, is not offering impartial advice in a fiduciary capacity in providing this sales and marketing material. This information is not meant as tax or legal advice. Investors should consult a professional advisor before making investment and financial decisions and for more information on tax rules and other laws, which are complex and subject to change.

The rate of return is used only to illustrate the effects of the compound growth rate and is not intended to reflect future values of the mutual fund or returns on investment in the mutual fund.